The current market conditions – the NASDAQ is down 28% year-to-date, and the S&P 500 is down 17% – offer bargain hunters a target-rich environment. Plenty of sound stocks have seen their prices decline, pulled down by the general market headwinds and the overall stock trend, to levels that have left them too cheap to ignore.

At this level, investors can find the benefits of cheap stocks, like those under $10, which offer both learning opportunities and huge upside potential. However, in evaluating stocks to buy, it is important to look at more than just the price.

Wall Street’s analysts are taking note, and are looking for the ‘Strong Buys’ among the market’s cheapest stocks. Some of their picks make interesting reading, and we’ve opened up the database at TipRanks to pull up the details on two of these stocks. These are equities priced under $10 per share, and Wall Street expects them to double or more in the year ahead. Here are details.

SkyWater Technology (SKYT)

We’ll start with a semiconductor chip company, the only fully US-owned pure-play silicon foundry in operation. SkyWater designs, develops, engineers, and manufactures semiconductor chips, and operated through the full process, from the computer models to the foundry floor. The company is based in Minnesota and uses a Technology as a Service (TaaS) model, offering customers a range of tech – including carbon nanotubes, power management, and photonics, as well as silicon chipsets – and the services to maintain it.

SkyWater went public in April of last year, in an IPO that bumped up investors’ hopes. The company sold about 8 million shares, and raised over $112 million in gross proceeds. Since then, however, SkyWater’s shares have dropped sharply, and are down 72% year-to-date.

In the past month, SkyWater has had some good news for investors. It announced a licensing agreement with Xperi in mid-May, gaining access to Xperi’s hybrid bonding technology to enhance its products capabilities. And, in early May, SkyWater reported total Q1 revenue of $48.1 million, beating expectations by ~$6 million, and showed a non-GAAP EPS profit of 5 cents, much better than the 33-cent loss expected.

Among the bulls is Craig-Hallum analyst Richard Shannon, who sees the fall in share price as an opportunity to get in on this stock. He

“[We] see the current price as an attractive entry point into this unique business model with high sales/GM improvement and potential tech moonshots… With continued growth and margin improvement, we see great potential for this stock over the next quarters and years. We believe we picked up this stock at the right time, and urge investors to take a strong look at this unique asset addressing long-term trends in semis and broader geopolitics,” Shannon opined.

These comments back up Shannon’s Buy rating, while his $10 price target implies a strong upside potential of ~122% for the year ahead. (To watch Shannon’s track record, click here)

Overall, SkyWater has 4 recent analyst reviews on file and they are all positive, giving the shares a Strong Buy consensus rating. The stock is priced at $4.51 and its average price target of $10 matches the Craig-Hallum view, with ~122% upside predicted. (See SKYT stock forecast on TipRanks)

Tactile Systems Technology (TCMD)

Next up is Tactile Systems, a company in the medical tech field. In a broad sense, Tactile Systems is working on new medical devices as treatments for chronic disease conditions. Getting into specifics, the company’s product line includes wearable prosthetics for the treatment of chronic swelling – lymphedema – of the head, neck, torso, and lower extremities.

Tactile stock is down 53% so far this year. While in part this can be attributed to the general market downturn, the company’s quarterly loss has likely not helped.

In the most recent report, for 1Q22, that loss deepened year-over-year. The current result, showed a non-GAAP loss of $5.4 million, compared to $3.1 million in the year-ago quarter; sequentially, the loss was roughly flat from Q4’s negative of $5.5 million.

The company did report solid results at the top line. Revenue grew from $42.8 million in 1Q21 to $48 million now – a y/y gain of 12%, and beating the forecast by ~6%. Gross profits were also up by 12%, while gross margins remained high at 70.6%. The company is looking forward to full-year revenues in the range of $235 million to $240 million, which would indicate growth in the range of 13% to 15% year-over-year.

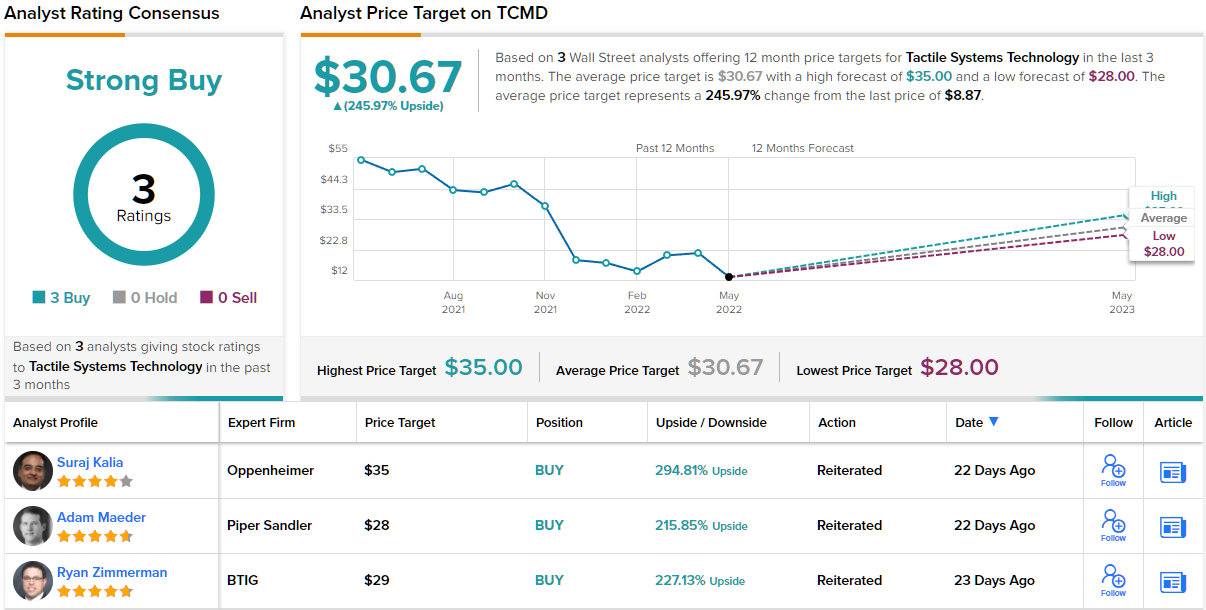

5-star analyst Adam Maeder is optimistic about Tactile’s future, based on its recent performance. He writes, “Tactile reported Q1 results that topped expectations on the top-line… Operational updates were largely positive as TCMD made good progress in Q1 rebuilding the salesforce and pushing forward the lymphedema pipeline. Bigger picture, this remains a commercial execution show-me story, however, the Q1 print marked a step in the right direction. TCMD trades a modest valuation, which we think provides an attractive entry point into shares — especially for those investors with longer-term investment horizons.”

Overall, Maeder thinks the stock has some way to go, and by some way, we mean 215% of upside. Those are the returns investors are looking at, should the stock make it all the way to Maeder’s $28 price target. No need to add, the analyst’s rating is an Overweight (i.e. Buy). (To watch Maeder’s track record, click here)

There are only three recent analyst reviews here, but they all agree that Tactile’s stock is one to buy, making the Strong Buy consensus unanimous. With shares priced at $8.87 and the average price target coming in at $30.67, this medical tech firm has an impressive 12-month upside potential of 246%. (See TCMD stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

This article was originally published on this site